CHARLEBOIS: The disappearing middle is distorting Canada’s food economy

Sylvain Charlebois writes, “You don’t fix food inflation by throwing money at it—you fix it by restoring a middle class that can actually afford to participate in the market.”

By: Dr. Sylvain Charlebois

Sylvain Charlebois is director of the Agri-Food Analytics Lab at Dalhousie University, co-host of The Food Professor Podcast and visiting scholar at McGill University.

Canada doesn’t just have a food inflation problem. It has a market structure problem—and it’s getting worse.

Over the past two years, we’ve been fixated on prices: why groceries cost more, why inflation remains stubborn, and why relief hasn’t materialized for many households. But we are missing the bigger issue. Canada’s economy is becoming increasingly K-shaped, and that is quietly undermining both affordability and innovation in our food system.

The data is unequivocal.

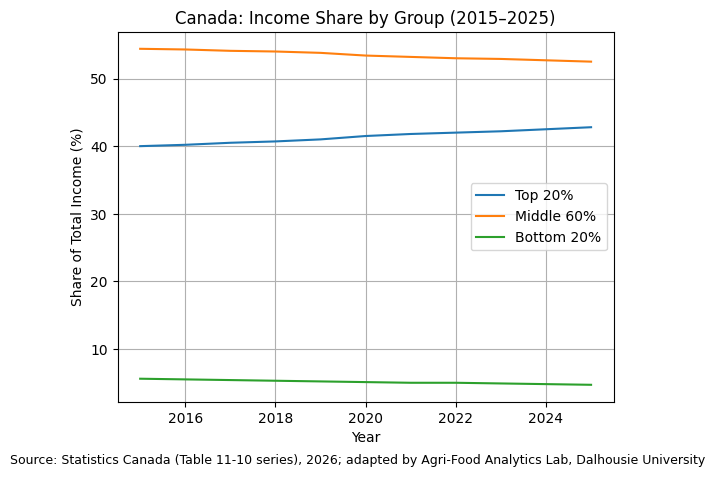

Over the past decade, Canada’s income distribution has shifted quietly but meaningfully. Data from Statistics Canada shows that the top 20% of earners increased their share of total income from roughly 40% in 2015 to nearly 43% in 2025, while the bottom 20% saw their share decline from about 5.6% to below 5% over the same period. As a result, the middle 60%—once the backbone of consumer demand—has steadily lost ground, with its share slipping by several percentage points

.At the same time, income growth is increasingly driven by financial assets, not wages. Higher-income households are benefiting from investment gains, while lower-income households are seeing their incomes lag behind rising costs. The result is a clear divergence: one group moving ahead, another falling behind, and a middle class slowly eroding.

This matters enormously for food.

A healthy food economy depends on a strong middle class. It is the middle that tries new products, supports emerging brands, and ultimately allows innovation to scale. Without it, the market fragments.

What we are now seeing is the emergence of two parallel food economies in Canada.

At the top, demand remains robust. Premium products, convenience, and value-added innovation continue to perform well. At the bottom, households are trading down aggressively, focusing on calories per dollar, often sacrificing quality, nutrition, and variety. Meanwhile, the middle—once the engine of growth—is shrinking.

This bifurcation has consequences.

First, it makes food inflation feel worse than it actually is. Official inflation numbers are averages, but they mask lived reality. Lower-income households spend a much larger share of their income on food and are more exposed to price increases. When prices rise—even modestly—they feel it more acutely.

Second, it makes inflation more persistent. When higher-income consumers continue to spend, there is less downward pressure on prices. At the same time, demand for essential goods among lower-income households is inelastic—they still need to eat. This combination creates a floor under prices that is difficult to break.

Third, and perhaps most importantly, it weakens innovation.

Without a strong middle class, companies face a difficult choice: innovate for the wealthy or cut costs for everyone else. What disappears is the space in between—the place where most meaningful, scalable innovation happens.

We are already seeing signs of this. Private label products are gaining ground. Retailers are becoming more risk-averse. Mid-tier brands are struggling to maintain shelf space. The system is not collapsing, but it is becoming less dynamic, less competitive, and ultimately less innovative.

And yet, the policy response remains largely focused on spending—subsidies, rebates, and temporary relief measures.

That approach misses the point.

Canada does not need to spend its way out of this problem. It needs to fix how its food market functions.

There are several reforms that would cost little, yet deliver meaningful impact.

Start with competition. Canada’s grocery sector remains highly concentrated. Stronger enforcement of competition laws—particularly around mergers, supplier relations, and exclusivity practices—would increase pressure on prices and create space for new entrants. This is where the new Grocer Code of Conduct will help.

Next, address internal trade barriers. It is still easier, in some cases, to import food from abroad than to move it across provincial borders. Harmonizing standards and removing interprovincial frictions would expand markets, reduce costs, and improve efficiency—without a dollar of new spending.

Regulatory simplification is another low-cost, high-impact lever. Aligning federal and provincial rules, speeding up approvals, and reducing duplication would lower compliance costs and allow innovation to reach consumers faster.

None of these measures are politically easy. But they are fiscally responsible—and increasingly necessary.

Because the risk is not just higher food prices.

The risk is that Canada’s food system becomes permanently divided: a premium market for those who can afford it, and a survival market for everyone else. That is not just an economic problem—it is a social one.

A K-shaped economy doesn’t just widen inequality. It changes how markets behave. It weakens innovation. It erodes resilience.

And in food, more than any other sector, that matters.

If we want a more affordable, innovative, and resilient food system, we need to stop focusing solely on prices—and start fixing the conditions that shape them.